The EV Boom and Beyond: Are Electric Cars the End Game?

The rapid expansion of the electric vehicle (EV) market is not just a global trend—it's a vital conversation that directly impacts Los Angeles and its businesses. With EV sales continuing to rise worldwide, accounting for nearly 18% of all car sales in 2023, the shift toward cleaner, more sustainable transportation is unmistakable. However, this growth is not without its challenges. Issues like vehicle costs, charging infrastructure, and electricity prices are slowing adoption in some regions, while others, such as Norway and China, are leading the charge with impressive adoption rates.

This is especially important for Los Angeles, a city known for its automotive culture and environmental initiatives, as well as many issues of air quality, traffic congestion, and climate change that are becoming increasingly concerning. The rise of EVs represents both an opportunity and a challenge. Businesses in Los Angeles, from local startups to large corporations, must adapt to a rapidly changing landscape.

This conversation is critical for several reasons: not only does the shift to EVs align with California's aggressive climate goals, but it also opens new avenues for innovation, infrastructure development, and market opportunities. From the expansion of charging stations to the development of new technologies like hydrogen fuel cells, Los Angeles businesses have the chance to play a pivotal role in shaping the future of transportation. As we explore the dynamics of EV market growth and the technological advancements shaping it, it's clear that Los Angeles is at the heart of this global transition, and its businesses must stay ahead of the curve to thrive in an increasingly electrified world.

While the overall trend of the production of EVs is certainly growing, we’ve also seen some slowdown in certain geographical areas. Sales in Denmark and Hong Kong faced a significant slowdown likely due to the phasing out of government subsidies. Declines in Italy and South Korea were attributed to various market conditions and changes in government policies.

On the other hand, when you look at countries like Norway, a staggering 93% of all new car purchases are EVs. This is closely followed by Iceland (71%), Sweden (60%), and Finland (54%). EV sales in China alone have reached 38% of the total market (8.1 million cars).

The USA, while being the leaders of innovation that bring new EV technologies to the forefront, are very much near the bottom of the sales curve. In the Q3 of 2024, only 8.9% of the USA market share was of EVs. While that is not a big number when compared to the numbers in Europe (or in China), that is still a record-high in comparison to previous years.

When looking more granularly, California continues to lead the charge in EV sales of every category, with 26% of all sales, trailed by other coastal states like Washington and Oregon.

But why is that? What is it about inland states that seems to cause these massive differences in comparison to their coastal neighbors? Why do EV sales in many of them fail to reach even 5% of market share?

Keeping many different details and geographical differences in mind, it seems like the three main factors that cause slowdowns in the EV market are:

Higher cost of vehicles

Charging opportunities

Cost of electricity

To address the first issue, many governments around the world, as well as US states, offered tax breaks or other incentives if people invested in an EV, and it definitely positively impacted sales. However, the very nature of government policy means this will likely only be a temporary measure. Once you break down the various production expenses, it becomes clear that EVs consistently cost more because their batteries are so expensive. On average, 40% of the entire price of an EV is just the cost of the battery.

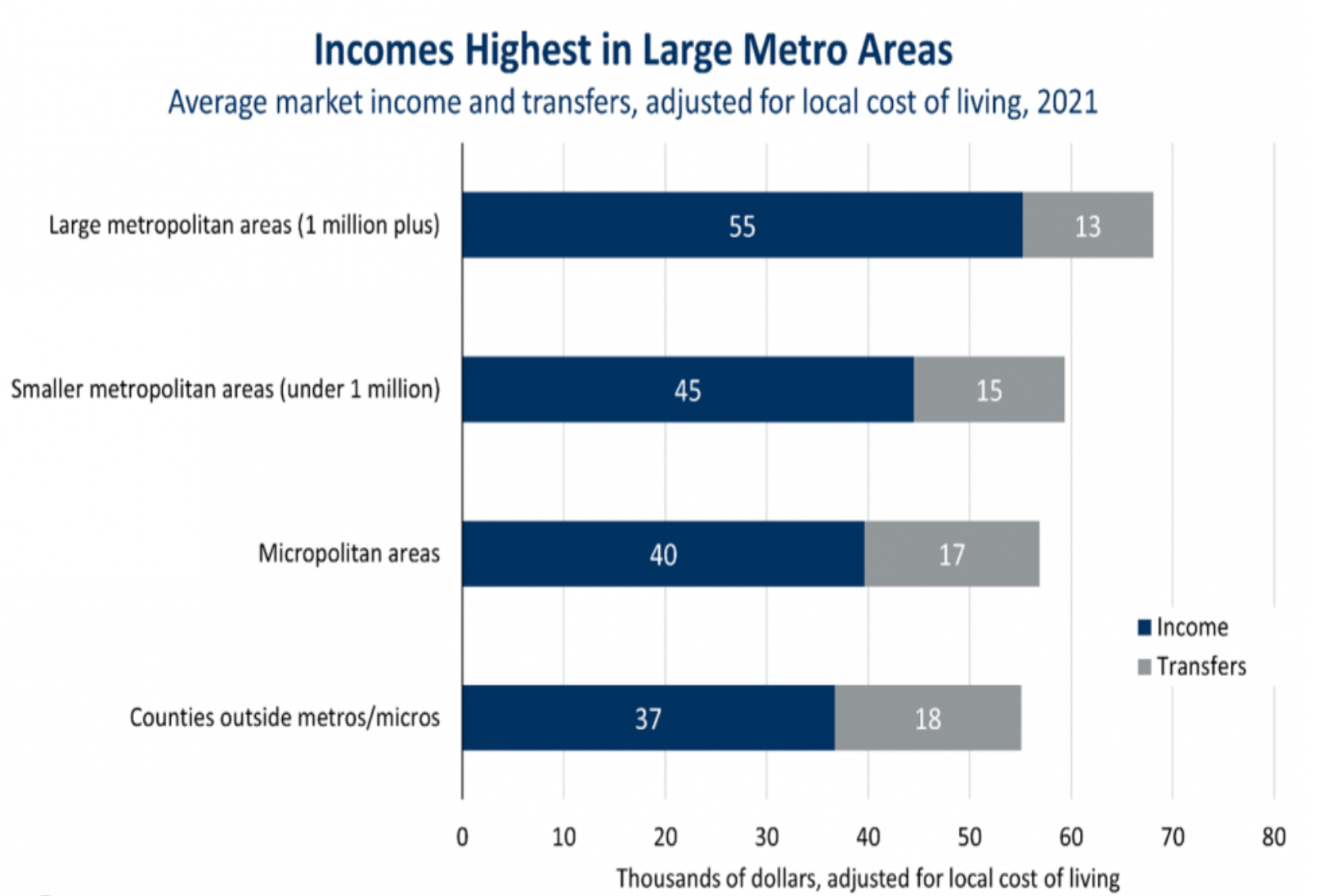

Once you realize that, it’s not a coincidence that higher-costing EV sales find more success in coastal US states. It is the result of geographic income inequality, which has risen more than 40% between 1980 and 2021 in the USA. This gap is large: incomes are 24% higher in large metropolitan areas than in smaller metropolitan areas, 39% higher than in micropolitan areas, and 51% higher than in counties outside of metropolitan and micropolitan areas. Many of the lowest-income communities are in rural America. Conversely, coasts are, on average, more populous and hold the bigger percentage of large metropolitan areas. Simply put, the highest concentrations of people who can afford EVs live on the coasts.

Charging availability and opportunity, on the other hand, is a two-fold issue. Public charging stations are not being created with not nearly enough speed and spread to meet with demand, and home charging is only possible for a small fraction of EV customers.

While the first issue can be addressed by targeted infrastructure investments (public and/or private), the second is subjectively based on circumstance. Home charging requires owning a property with a private garage that can support either a dedicated charging station for single family homes, or a network of stations that are able to serve the entire population of a condominium. Office charging also requires employee garages with the proper support. In cities like Los Angeles, where a very significant portion of the population lives in multi-unit buildings (about 44%), many where only street parking is available, neither option is feasible.

The cost of electricity also differs widely by state (and country), and definitely has a serious impact on the decision to buy an EV considering the local gas pricing. China beats most of Europe as well as the United States, with an average cost of $0.08 per kilowatt-hour (compared to the USA’s average of $0.26), which obviously reflects in their sky-high EV sales.

What is interesting to note though, is that within the US, costs for electricity on the coasts are much higher than in the flyover states (highest is Connecticut with an average of $0.33/kWh and lowest is Louisiana with an average of $0.12/kWh). This would make one assume that it would impact sales in the opposite manner. This is where the geographical income gap comes heavily into play again, as well as the ever-increasing tendency for aggressive political smear campaigns against EVs.

Innovations in technology can unfortunately only address some of these challenges. In recent years, we’ve had several improvements and breakthroughs on battery design. We now have several new battery technologies (solid state, Sodium-ion, Lithium-Sulfur, Graphene, etc.) that promise faster charging times, a longer life cycle, and lower costs. Some of them are already in production, others will go on the market soon. In the end, if you look at the span of time that cars have been in existence (first car was created by Carl Benz in 1885), EVs have been commercially available hardly a handful of years (Nissan Leaf, 2010) compared to a century old ICE car technology. So all things considered, we have come a long way very quickly and we have a long way still to go.

Even if this is entirely encouraging, the question remains. Will EV be the long-range solution for the transportation of the future?

My opinion is no.

EVs are a necessary step toward the end of the harmful monopoly of the fossil fuel industry, but I don’t think they are the final solution. To even hope of matching the maximum mileage range of modern ICE cars, EV batteries will need to get bigger and bigger. No matter how much improvements in battery technology may impact this, an increase in size will equate to ever-lengthening charging times, which will never be able to fully compete with the efficacy and speed of an old-fashioned gas fuel-up.

If you add that together with the longstanding complex societal and infrastructural issues that I discussed above, I personally feel hydrogen (fuel-cell) based engines are actually the ones we are starting to see promising samples of in the real market.

But what is a fuel-cell-based engine (FCEV)?

FCEVs use a propulsion system similar to that of electric vehicles, where energy stored as hydrogen is converted to electricity by the fuel cell.

As usual, any new propulsion technology that hopes to be appealing to the market requires a robust refueling infrastructure and there is still too much of a shortage of hydrogen stations to make them comparable to ICE or EVs right now. But just like when EVs were new to the market, we are slowly getting there.

The advantages of a fuel-cell engine are many:

We do not need a huge, heavy, costly battery, just a small one

The emission is just vapor

Charging is a pretty quick procedure

Hydrogen is available everywhere

No matter how exciting this all is for the future of sustainable transportation though, there are still some challenges to overcome:

The current technology still requires bulky gas tanks

Difficulties in hydrogen storage and production

Concerns about safety

The great this is that all of these are issues that technology can absolutely assist with. Just recently, news has come about about breakthroughs in tank design and hydrogen storage. Instead of a big bulky tank the option is to provide the car with many (4-6) small removable tanks, similar to big coffee thermos. You can easily replace them at a refueling station or even have them delivered at home. Charging becomes almost instantaneous. Toyota is already offering such a solution to any vehicles that are created with this design, and the NamX HUV is a concept car that is already implementing it.

Toyota, Honda and Hyundai already have commercially available fuel cell based cars (the Mirai, Nexo and CR-V(2025)). Prices are between $50K and $60K, which is already comparable to top-of-the line EVs on the market now, and we can only expect prices to go down as research advances and production methods are improved upon and streamlined.

We already have decades of experience in installing and managing removable gas tanks (e.g. LPG or Methane) in modern-day vehicles, so it should not be an issue in terms of safety.

Advances in hydrogen production have also been in the news lately. At the moment, Hydrogen production is quite expensive and not efficient, driving the retail price to an average of $16/Kg (California). Considering an average of 66 MPGe (Mileage Per Gallon equivalent), it’s around 2.5 times more expensive than gasoline (in California).

But once again, innovators are already well on their way to doing what they do best: solving the problem, which is impressive considering the relative youth of the technology.

An Italian startup, Green Independence, for example, is proposing a very efficient and cheap method to produce hydrogen as a side product of the water desalination process. They promise to bring the hydrogen production cost from $10/Kg to $1/Kg.

We just need to give them a chance to prove themselves right.